- Selling

- Buying

- Landlords

- Renting

- New homes

- House prices

- International services

International offices

International offices

China, Hong Kong SAR, India, Indonesia, Malaysia, Middle East, Pakistan, Qatar, Singapore, South Africa, Thailand and Turkey

Learn more - News

- Contact

- About us

- My B&R

UK Landlords face 200% penalty for unpaid tax

|

Getting your Trinity Audio player ready...

|

Landlords need to be very careful and sure they have declared all their property income on their UK tax returns and paid all monies due. Whether an underpayment is intentional or not, HMRC can now collect the tax due PLUS interest PLUS impose a whopping 200% fine.

Landlords need to be very careful and sure they have declared all their property income on their UK tax returns and paid all monies due. Whether an underpayment is intentional or not, HMRC can now collect the tax due PLUS interest PLUS impose a whopping 200% fine.

The UK Government is putting pressure on HM Revenue and Customs (HMRC) to collect as much tax as possible. Accordingly, the HMRC are intensifying their efforts to ensure compliance among all landlords and HMRC are tasked with ensuring every penny of tax that is due, is paid promptly. Gone are the days when a landlord who gets caught under-declaring could rely on just paying interest. Today, HMRC have the power to charge up to 100% as a penalty – landlords must be warned that this fine is in addition to the tax that’s due plus interest on the tax. And even worse for any landlords lucky enough to earn overseas income, then the maximum fine could be an eye-watering 200%!

HMRC are currently reviewing all landlords tax liabilities. The aim of the review is to ensure that landlords pay the correct amount of tax due and any discrepancies be investigated, identified and paid. The focus is on a range of tax matters, including income from property rental, capital gains tax and inheritance tax. It will also examine the use of allowances and deductions by landlords. The crackdown on landlords comes as part of HMRC’s wider efforts to increase tax compliance across all sectors of the economy. HMRC are focusing on areas where it believes tax evasion is most prevalent and easiest to collect which means the primary target is buy-to-let landlords.

So How does HMRC track rental income?

HMRC has several methods of accessing this information, including via local authories (councils), online platforms (properties listed on portals such as Rightmove, Zoopla), public records, data-sharing agreements with other government agencies, information from banks directly, letting agents and referencing agencies. HMRC are now using data analytics software which uses a range of sources like property websites, land registry and tenant referencing agencies. They also gather information through third-party reports such as mortgage interest and bank statements.

On the flip side, HMRC don’t only use a stick to encourage compliance, they do targeted campaigns to encourage landlords to declare their rental income, and if declared voluntarily HMRC have the flexibility to reduce and even waive fines. HMRC carry out random checks and investigations and woe-betide a landlord who is caught as this could lead to a lengthy investigation into their tax affairs dating back several years and if they spot any discrepancies, they will apply the maximum possible penalties.

How much tax do landlords need to pay, and what is the penalty for defaulters?

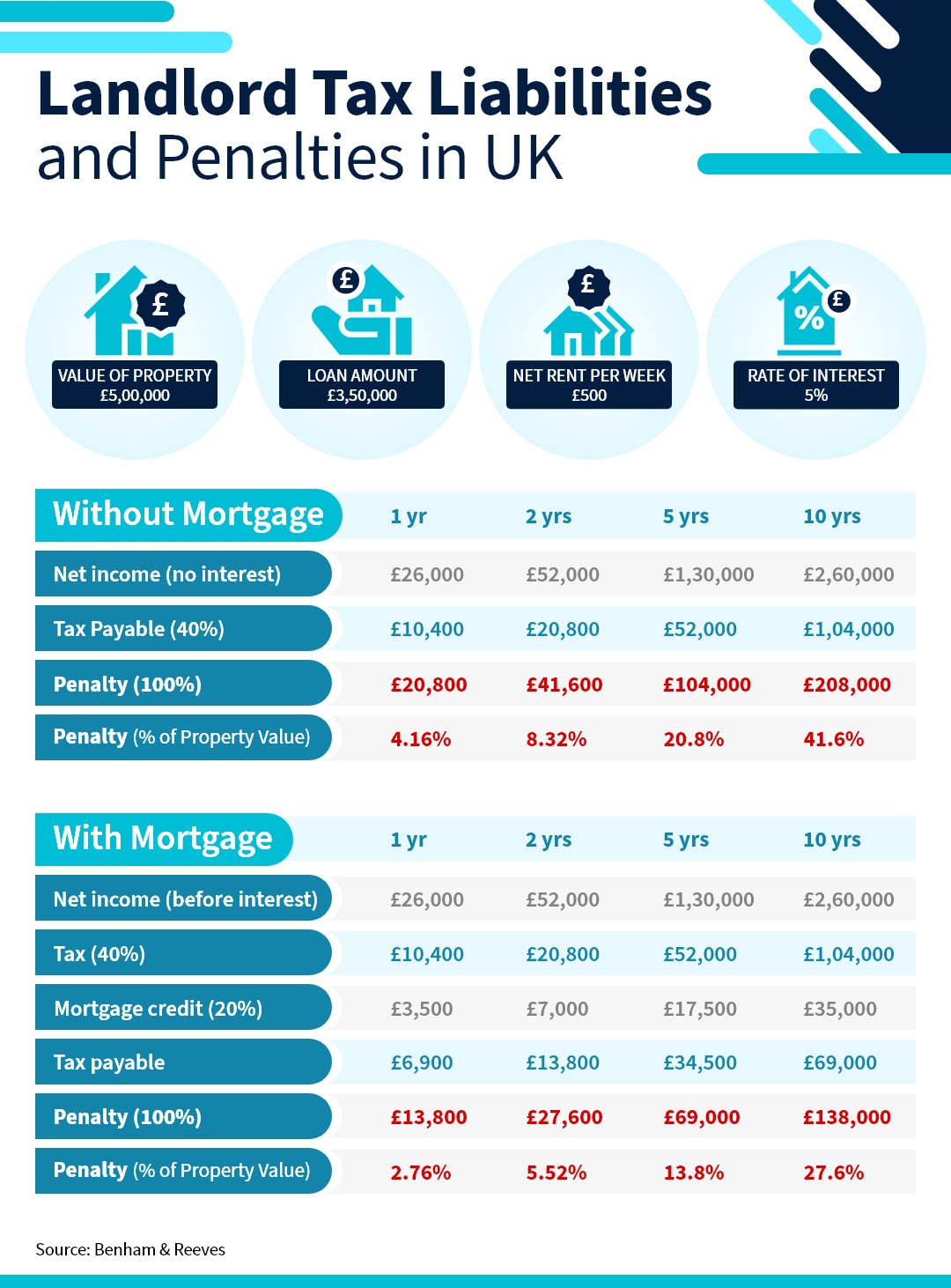

To understand the tax amount a landlord is liable to pay on their rental property income, it’s useful to consider an example – for the purposes of this example we used the following:

– A property in London valued at £500,000

– No loan/mortgage

– Rental of about 5% – which is £500 per week which is £26,000 per annum

– Taxpayer is based overseas

– Taxpaper is paying tax at the higher tax rate

So taking into account the above, the tax would be 40% of the rent – £10,400 per annum

tax.

If the landlord fails to accurately declare, then HMRC can fine the landlord 100% of the taxable amount. Plus interest backdating to the date the tax was due. In this case therefore fine would be £10,400 plus interest plus tax £10,400 – that’s going to come to over £21,000– that’s almost the entire rent! But had a landlord not declared any rental income for 10 years, the amount inclusive of the tax due, fines and interest could add up to a whopping £230,000– not only does this mean all the income is wiped out, but worse still, it represents 45% of the property’s value which is disaster surely for landlords! The situation could be even worse if the landlord was an additional tax rate payer i.e. paying 45% tax rate – then the bill over 10 years could be as much as £250,000 with tax, fine and interest – that’s 50% of the property value!

But a landlord had not declared any rental income for 10 years, the amount inclusive of the tax due, fines and interest could add us to a whopping £230,000– not only is that meaning all the income is wiped out but worse it represents 45% of the property’s value. Disaster surely for landlords!! The situation could be even worse if the landlord was an additional tax rate payer ie paying 45% tax rate – then the bill over 10 years could be as much as £250,000 with tax, fine and interest – that’s 50% of the property value!

And can you imagine if the Landlord has overseas income too – then the fine could be 200% and over 10 years then that would represent almost 75% of the property’s value, so it’s vital not to be informed of your liability and ensure compliance.

This is clearly a worse case scenario – but we provide some more examples below based on one, five and ten years, both with and without a loan – but whichever case a landlord considers, no-compliance is a no go, the HMRC will catch up with you in the end and when they do, they have very draconian powers and will pursue landlords wherever they are until everything has been paid.

How far back can HMRC investigate rental income?

HMRC can investigate property rental income records as far back as they deem necessary if it suspects a deliberate tax evasion – they view this as criminal activity and will pursue until they collect.

HMRC do issue “nudge” letters to landlords they suspect for irregularities asking the landlord to be transparent and provide all information to avoid heavy fines. Landlords would be foolish to ignore any such correspondence as they will be far more aggressive will likely lead to a full investigation of your affairs with HMRC reviewing all aspects of a landlord’s income, including income earned via non-rental sources as well.

Can unpaid tax be declared to reduce liability?

The ‘Let Property Campaign’ initiated by HMRC gives all UK landlords a chance to bring their tax affairs up to date. Under this scheme, landlords with undisclosed rental incomes have 90 days to calculate and pay the tax liable on their rental incomes.

Since this is a voluntary disclosure by landlords, HMRC are highly likely to reduce the penalties or fines. The benefits of this scheme can only be availed by individual landlords letting out residential properties and do not apply to companies or trusts with undisclosed rental incomes. Honesty and openness is always the best way forward.

How to reduce rental tax liability and avoid penalties?

Transparency in declaring rental income is the first step for all landlords to ensure taxes are minimised.

Our examples don’t take into account expenses. Claiming allowable expenses like repairs, maintenance costs, utility bills and insurance premiums are simple way reduce a landlord’s tax liability.

In summary, the net is closing in and any landlords evading tax by not declaring their income are running a very serious risk. With the cost of living crisis and the UK’s government need to cover the costs of the Covid pandemic, anyone not paying tax due will be pursued and landlords are a key target for HMRC as property values are high and can be sold to cover taxes and fines.

We recommend that Landlords take professional advice to ensure their income is correctly reported, minimising a landlord’s tax obligation to avoid interest and punative fines. Moreover, by being transparent, a landlord reduces the risk of an HMRC investigation which will be very meticulous, time consuming and expensive if you need accountants or lawyers to step in and assist.

If you are an overseas investor and need assistance with completing a tax return, we can help. Get in touch with our tax return team for further details.

Sign up to our newsletter

Subscribe

How much is your property worth?